Compare life insurance quotes*

Compare life insurance with Australia’s leading providers

Call 1800 717 485

Free quote comparison in 30 seconds

What does it cost?

Our comparison tool is completely free to use and we don’t charge any implementation fees. Your only expense is the premium which can be funded from your superannuation fund or personally.

3 Easy Steps

1

Choose your cover

Select the appropriate cover for your circumstance. Choose between Life Cover, Income Protection, TPD and Trauma.

2

Compare

Compare product features and premiums from Australia’s leading insurance providers.

3

Implement

Work with our expert team to understand the different features and apply for your cover.

Learn more about life insurance

Insurance premiums paid from Superannuation

Life Cover, TPD Cover and Income Protection premiums may be deducted from your super balance and you don’t need to change your superannuation fund.

The costs of insurance premiums come out of your super account, so you won’t be dipping into your take-home pay.

Income Protection

Pays you a monthly benefit to replace part of your income if you are temporarily unable to work as a result of serious illness or injury. Allows you to cover everyday living expenses and maintain the lifestyle you’ve built for yourself and your loved ones.

There’s not much you can do without an income. In monetary terms, your ability to earn an income is your biggest asset by far – which is why Income Protection is so important.

Trauma Cover

Pays you a lump sum in the event of certain types of serious illness or injury like cancer, heart-attack and stroke.

It allows you to cover the cost of out-of-pocket medical expenses and financially support your lifestyle and family during an extended break for you from work as you recover.

Life Insurance

Pays a lump sum to your beneficiaries or estate in the event of your death or terminal illness. Allows you to pay off any existing debts, cover living expenses for your dependants, or provide the financial support you’d like to give them in your absence.

It may be the simplest form of life insurance, but life cover is undoubtedly one of the most important as it helps you provide for your dependants.

Total and permanent disability (TPD)

Pays you a lump sum if an illness or injury leaves you permanently disabled and unable to work, or perform normal domestic duties if you work in a home-maker role.

Allows you to cover out-of-pocket medical expenses, home or transport modifications, support your ongoing financial needs and take care of your dependants.

What's the right amount of cover?

There are three important things to consider:

- How much would you require to pay off any existing debts?

- What would be the cost of living for you and your loved ones during a recovery from an incident that changes your lives to the extent where you can’t work?

- How much would you need for the financial security of your dependents and the life you wish for them – including the cost of their education and continued living expenses?

Frequently Asked Questions

Can I pay for my Life Insurance through Superannuation

Your superannuation fund is able to hold Life Cover, TPD Cover and Income Protection. With this option, your premium is deducted from your super balance, and you don’t need to change your superannuation. The costs of insurance premiums comes out of your super.

Why do I need Life Insurance?

Life insurance is a financial tool designed to provide a measure of financial security for your loved ones in the event of your death. While it may not be necessary for everyone, there are several reasons why individuals often consider getting life insurance:

1.Financial Protection for Dependents: If you have dependents, such as a spouse, children, or other family members who rely on your income, life insurance can help replace that income in case you pass away. This can be crucial to ensure their financial well-being, covering expenses like mortgage payments, education costs, and daily living expenses.

2.Debt Coverage: Life insurance can be used to pay off outstanding debts, such as a mortgage, car loans, or credit card debt, preventing your loved ones from inheriting financial burdens.

3.Funeral Expenses: Funerals can be expensive, and life insurance can help cover the costs, sparing your family from the financial burden during an already difficult time.

4.Estate Planning: Life insurance can be a valuable component of estate planning, providing liquidity to cover estate taxes, settlement costs, and ensuring that assets are passed on to your heirs as intended.

5.Business Protection: If you own a business, life insurance can be used to fund a buy-sell agreement, ensuring a smooth transition of ownership in the event of your death. It can also be used to protect the business from financial losses associated with the death of a key employee.

6.Peace of Mind: Knowing that your loved ones will be financially protected in case of your untimely death can provide peace of mind. It allows you to focus on your life knowing that you’ve taken steps to secure your family’s financial future.

7.Affordability: Life insurance premiums are often more affordable when you’re younger and healthier. By getting a policy earlier in life, you may lock in lower rates.

Why do I need Total and Permanent Disability Insurance?

Total and Permanent Disability (TPD) insurance is a type of coverage that provides financial protection in the event you become totally and permanently disabled and are unable to work. Here are some reasons why you might consider having TPD insurance:

1.Financial Security: TPD insurance provides a lump-sum payment if you experience a total and permanent disability. This financial support can help cover medical expenses, rehabilitation costs, and daily living expenses during your recovery.

2.Debt Repayment: The lump-sum payment from TPD insurance can be used to repay outstanding debts, such as mortgages, car loans, and credit cards. This can prevent financial strain on you and your family during a challenging time.

3.Lifestyle Maintenance: A TPD insurance payout can assist in maintaining your lifestyle by covering ongoing living expenses, including utility bills, groceries, and other essential after costs

4.Modification of Living Arrangements: If your disability requires modifications to your home or living arrangements, the funds from TPD insurance can be used for these purposes. This may include installing ramps, modifying bathrooms, or making other accommodations to improve accessibility.

5.Cover Gaps in Other Insurance: While health insurance may cover medical expenses, it might not provide sufficient funds for long-term disability-related costs. TPD insurance can fill these gaps and offer a more comprehensive financial safety net.

6.Quality of Life: TPD insurance can contribute to maintaining your quality of life by providing financial resources for activities and experiences that enhance well-being, even in the face of a permanent disability.

7.Support for Dependents: If you have dependents, a TPD insurance payout can provide financial support for their ongoing needs, including education, childcare, and other expenses, lessening the impact of your disability on their lives.

8.Supplementing Income Replacement: If you have income protection insurance, TPD insurance can complement it by providing a lump sum that can be invested or used strategically to supplement ongoing income replacement during a period of disability.

9.Peace of Mind: Knowing that you have financial protection in place in the event of total and permanent disability can offer peace of mind. This assurance allows you to focus on your recovery without the added stress of financial uncertainty.

Why do I need Trauma Insurance?

Trauma insurance, also known as critical illness insurance, is a type of coverage that provides a lump-sum payment if you are diagnosed with a specified critical illness or medical condition. Here are several reasons why you might consider having trauma insurance:

1.Financial Protection for Critical Illness: Trauma insurance provides a financial safety net in the event you are diagnosed with a critical illness covered by the policy. This lump-sum payment can help cover medical expenses, rehabilitation costs, and other financial needs during your treatment and recovery.

2.Cover Gaps in Health Insurance: While health insurance covers medical treatments, it may not cover all expenses associated with a critical illness. Trauma insurance can fill these gaps, providing funds for various needs beyond medical bills.

3.Quality of Life: The lump-sum payment can be used to enhance your quality of life during and after treatment. This may include funding special treatments, travel for medical care, or pursuing activities that contribute to your overall well-being.

4.Non-Income Replacement: While Income Protection insurance is designed to replace lost income due to disability, trauma insurance provides a lump sum regardless of your ability to work. This means you receive a payout even if you can still work but are dealing with significant medical expenses or lifestyle changes.

5.Choice and Flexibility: The flexibility of a lump-sum payment allows you to decide how to use the funds based on your specific needs. This gives you the freedom to allocate the money where it is most beneficial for you and your family.

6.Debt Repayment: The lump-sum payment from trauma insurance can be used to repay debts, such as mortgages, loans, or credit card balances. This can help ease financial stress during a challenging time.

7.Peace of Mind: Knowing that you have financial protection in place if you face a critical illness can provide peace of mind. It allows you to focus on your recovery and well-being without the added worry about the financial implications of your medical condition.

What is the difference between Workers’ Compensation and Income Protection?

Workers’ compensation and income protection are both types of insurance that provide financial support to individuals in the event of certain risks or challenges, but they serve different purposes and cover distinct areas. Here are the key differences between workers’ compensation and income protection:

1.Purpose and Coverage:Workers’

Compensation: This type of insurance is specifically designed to provide benefits to employees who suffer injuries or illnesses while on the job. It typically covers medical expenses, rehabilitation costs, and a portion of the injured worker’s lost wages.Income Protection: Income Protection insurance is broader in scope. It is designed to replace a portion of an individual’s income in the event they are unable to work due to illness, injury, or disability, regardless of whether the condition is work-related or not.

2.Eligibility:Workers’

Compensation: Eligibility is based on the fact that the injury or illness occurred while the individual was performing job-related duties.Income Protection: Eligibility is generally based on the policyholder’s ability to work and earn income, regardless of where the injury or illness occurred.

3.Benefit Structure:

Workers’ Compensation:

Benefits may include medical treatment, rehabilitation services, and a portion of the worker’s wages during the period of disability. The amount is often set by state laws.Income Protection: Benefits are typically a percentage of the policyholder’s pre-disability income. The policyholder may receive regular payments until they recover and return to work, reach a specified age, or for a predetermined period, depending on the policy terms.

In summary, workers’ compensation is a specialised insurance that focuses on workplace injuries and illnesses, while Income Protection is a broader form of coverage that provides financial support in the event of disability or illness, whether work-related or not.

Why get insurance through Life Cover Compare rather than direct?

Direct insurance provides limited coverage, your premium increase with age, and underwriting is only done at the time of claim, which results in a higher percentage of claims being rejected. Appyling for cover through Life Cover Compare will ensure that your policy is underwritten at the time of application and our guidance will help you chose the best cover for you. The products that we compare provide extensive cover which means you can be sure of better insurance coverage with lower premiums and a high claim approval rating.

Is purchasing insurance directly cheaper?

Overall, no. Direct insurance products offer limited features and benefits and restrict your premium payments options as you age, meaning you pay more as time goes by. Retail insurance products provide more cover and are better suited to your needs for less money.

What do I need to consider with Life Insurance?

When you’re looking at life cover, there are 3 key things you need to understand so you know what will happen at claim time:

1.How much you’re covered for

2.How your policy will be paid out

3.How your cover is structured – linked or stand-alone

How much you’re covered for?

It might sound obvious, but you need to think about the reasons you take out life cover when you apply for cover. You might think “$1 million should be enough” – but have you thought about how much money would really be needed to replace your income, support your family, educate your children etc.?

The Australian Securities and Investments Commission (ASIC) has developed a Life insurance calculator that can help.

How your policy will be paid out?

When a life cover benefit is paid, it’s generally paid to the owner of the policy or a nominated beneficiary. In many cases the policy owner will be your spouse or your estate. But what if your policy is owned inside super?

In this case, the policy owner is the trustee of the super fund – meaning they receive your benefit from the insurer. The trustee will then pay your benefit to the beneficiary(s) you’ve nominated, or your estate.

How your policy is structured – linked or stand-alone?

Life cover may be purchased as a stand-alone policy or as a ‘linked policy’ that’s connected to TPD cover or trauma cover. Linking policies reduces your premium, but there are implications at claim time.

Say you have a $1 million life cover policy linked to a $500,000 TPD cover policy. If you make a successful claim on your TPD cover, your life cover benefit will reduce by the $500,000 paid out.

Depending on your situation you may be eligible to buy back this extra life cover at some point, but it’s important to note that your life cover is significantly reduced in the meantime.

What do I need to consider with Income Protection?

There’s not much you can do without an income. In monetary terms, your ability to earn an income is your biggest asset by far – which is why Income Protection is so important. When you’re protecting your biggest asset, there are 3 things you need to understand so you know what you’re covered for, and what that means at claim time:

- How much you’re covered for – the sum insured

- How long you need to wait to be eligible to make a claim – the waiting period

- How long your claim will be paid for – the benefit period.

- Sum insured

When you apply for Income Protection, you can generally choose a sum insured that’s up to 70% of your before-tax income (excluding super contributions).

- Waiting period

The waiting period is the number of days before you become eligible to claim, starting from the date the doctor confirms you are disabled. The most common chosen waiting period options are 30 days, 60 days, 90 days and 2 years.Income Protection payments are usually made monthly in arrears. So, if you had a 30-day waiting period, your first payment would be made 60 days after you first became disabled.The waiting period affects the premium. Naturally, a policy with a 30-day waiting period is more expensive than the same policy with a 90-day waiting period, because you’re eligible to claim sooner.When choosing your waiting period, you should think about how soon you’re likely to need financial support if your income stops:

– If you have access to sick leave or annual leave, or a high level of savings, you may be able to take a longer waiting period and reduce your premium.

– If you’re a business owner, or you have a low level of savings, you may want a shorter waiting period, bearing in mind your premium will be higher.

- Benefit Period

The benefit period is the maximum amount of time you can receive Income Protection payments for any claim while you are disabled. It can be based on time (e.g. 2 or 5 years) or age (e.g. to age 65).

Say you’re aged 40 and you become permanently disabled, meaning you’ll never be able to return to work. If you had a 2-year benefit period, your benefit payments would stop when you’re aged 42. But if your benefit period was to age 65, you would continue to receive benefit payments for an additional 23 years as you continue to meet the disability definition.Choosing a longer benefit period increases your premium because the potential payout is higher. However, be aware the benefit period is the maximum amount of time you can receive payments. If you’re able to return to work sooner than that, or you reach age 65, your payments will stop.Also, if your policy offers ‘partial disability benefits’, you may be able to return to work part-time and receive reduced payments until you’re able to work to full capacity. This can be a great benefit to have as it means you’re supported if you’re restricted in your capabilities, or you want to try a new occupation.

- Sum insured

What do I need to consider with Total and Permanent Disabled (TPD) Insurance?

A permanent disability will change what the rest of your life looks like. It can also make life much more expensive in terms of medical care and home modifications – which is why TPD cover is so valuable. When you’re looking at TPD cover, there are 3 key things you need to understand so you know what you’re covered for, and what that means at claim time:

- How your claim will be assessed – Any or own occupation

- How long your claim will take – Maximum medical improvement

- How your cover is structured – Stand-alone or linked

- Any or own occupation : When you start a TPD cover policy, you may be given a choice of definition that will apply at claim time. The two main choices are: Own occupation – Where your claim is assessed against your ability to perform the specific requirements of the job you currently do, or Any occupation : Where your claim is assessed against your ability to perform any job you are qualified or suited to based on your education training or experience.

Say you’re a cabinet maker who permanently loses the use of one of their hands. Under an own occupation definition, you’re likely to be considered totally and permanently disabled as you’ll never be able to perform your current job again. But under an any occupation definition, you may still be able to work for a building supply company providing advice which means you may not be considered totally and permanently disabled. With a greater likelihood of a claim being accepted, an own occupation definition typically adds to the cost of TPD, and it may not be available to all occupations.

- Maximum medical improvement: TPD cover claims can take longer to pay than other types of life insurance, mainly because of the complexity involved in determining whether a disability is permanent.Generally, a TPD claim will only be paid when you obtain “maximum medical improvement”. That means you need to have had any operations, rehabilitation or medical procedures recommended by your treating doctors.As you can imagine, a TPD cover claim can take months or even years to play out, and it does have a higher decline rate than other cover types because of the difficulty in proving permanency. For those reasons, TPD cover is often taken in conjunction with trauma cover – which can provide more immediate financial support for a defined list of serious medical conditions.

- Linked covers: TPD cover may be purchased as a stand-alone policy or as a ‘linked policy’ that’s connected to life cover or trauma cover. Linking policies reduces your premium, but there are major implications at claim time.Say you have a $200,000 TPD cover policy linked to a $500,000 life cover policy. If you make a successful claim on your TPD cover, your life cover benefit will reduce by the $200,000 paid out (i.e. to $300,000).

What do I need to consider with Trauma Insurance?

Trauma cover is all about supporting your recovery from a serious illness – helping you afford the treatment of your choice and allowing you to make necessary changes to your lifestyle. When you’re looking at trauma cover, there are 3 key things you need to understand so you know what you’re covered for, and what that means at claim time:

- What you can claim for – Trauma definitions

- How your cover is structured – Stand-alone or linked

- Making multiple claims – Trauma reinstatement

1.Trauma definitions

Every trauma cover policy comes with a list of definitions that dictates:- what medical conditions are covered by your policy

– how severe those conditions need to be for a claim to be paid

– what percentage of the sum insured will be paid in the event you suffer one of the covered conditions.

Generally speaking, trauma cover is designed to cover you for severe conditions that are likely to require expensive medical treatment, a significant recovery period and/or force you to make major lifestyle changes. It is not designed to cover you for minor conditions that require simple or non-invasive treatments.

For example, you may be diagnosed with a skin cancer that hasn’t spread and is treatable in one procedure. Or you may be diagnosed with an aggressive skin cancer that requires chemotherapy or radiotherapy for months. They’re both technically ‘skin cancer’, but they’re very different in terms of their impact on your life.

You can find the trauma definitions that apply to your policy in the Product Disclosure Statement (PDS), with many of these definitions now standard across the life insurance industry. It is worth reviewing and understanding the differences between policies to ensure you get the best cover for you and your loved ones.

2.Linked covers

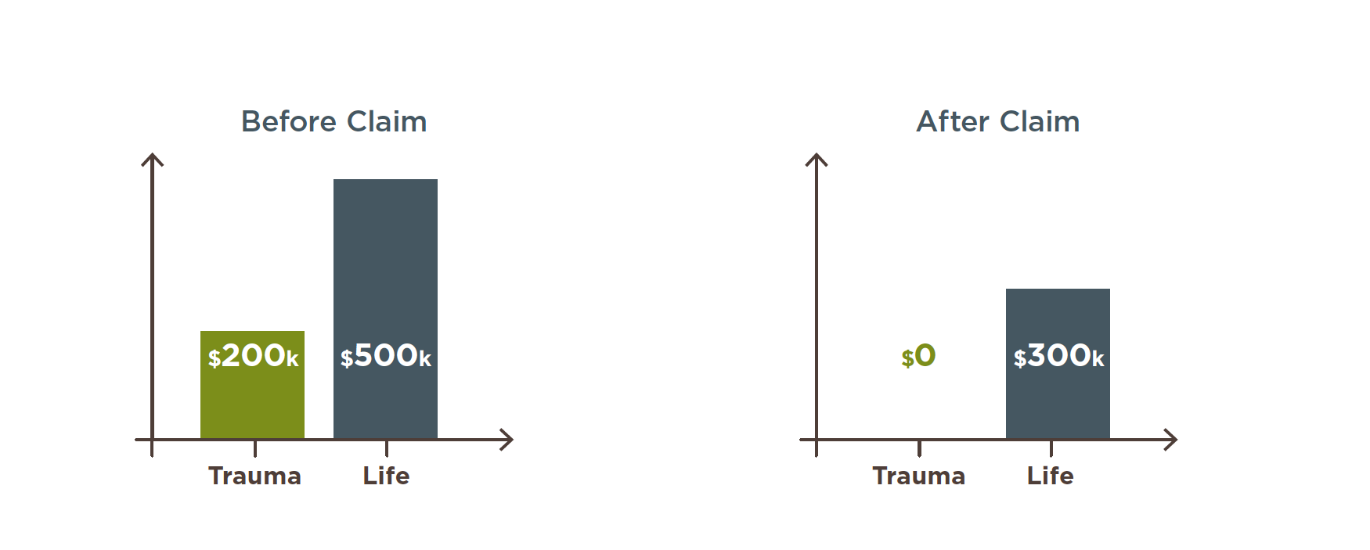

Trauma cover may be purchased as a stand-alone policy or as a ‘linked policy’ connected to life cover or TPD cover.Generally linking policies reduces premiums, but there are implications at claim time. Say you have a $200,000 trauma cover policy linked to a $500,000 life cover policy. If you make a successful claim on your trauma cover, your life cover benefit will reduce by the $200,000 paid out (i.e. to $300,000).

Depending on your situation you may be eligible to buy back this extra life cover at some point, but it’s important to note that your life cover is significantly reduced in the meantime.

3.Trauma reinstatement

A little-known benefit of trauma cover is that you may be able to make multiple claims in your lifetime.That’s because some trauma cover policies offer a trauma cover reinstatement option after a successful claim. A reinstatement option allows you to recommence your policy, typically 12 months or more after a claim has been paid. Typically, a reinstated policy won’t cover you for the same medical condition you already claimed on, or a related condition, but it can still cover you for a wide range of other serious illnesses.

Learn more about Trauma insurance and it’s exclusions in the Product Disclosure Statement, otherwise speak to your financial adviser.

What does it cost?

Our comparison tool is completely free to use and we don’t charge any implementation fees. Your only expenses are the cost of the premium which can be funded from your superannuation fund or personally.

Do you have any helpful links?

Further information on insurance, including tools and resources, are available through the Australian Government’s MoneySmart website here (https://moneysmart.gov.au)